Divorce often means sorting through years of shared decisions, shared goals, and shared accounts. Retirement assets can be one of the most important pieces to address because they are often substantial, governed by special rules, and easy to mishandle without a clear process.

This guide walks through how retirement accounts are typically identified, valued, and divided during divorce. We’ll cover the different plan types, the paperwork involved, the tax issues to watch for, and the practical steps that can help you move forward with greater clarity and fewer costly mistakes.

Key Takeaways

Dividing retirement accounts in divorce is rarely as simple as splitting a balance in half. Different plans follow different rules, and timing, paperwork, and tax treatment all matter.

Having a clear understanding of the process can help you stay organized, protect what you are entitled to, and reduce the chance of delays or unexpected consequences later.

- Different retirement plans are divided in different ways. A 401(k), pension, IRA, and governmental plan do not follow the same procedures.

- Usually, only the marital portion is divided, not necessarily the full account balance.

- Employer-sponsored plans often require a Qualified Domestic Relations Order, or QDRO, before benefits can be transferred.

- IRAs and Roth IRAs are usually divided through a transfer incident to divorce, not a QDRO.

- Errors in paperwork, timing, or distribution method can create taxes, penalties, or preventable delays.

- Starting early and seeking plan pre-approval when available can make the process smoother.

When you understand the fundamentals before decisions are finalized, it becomes easier to approach the rest of the process.

What Is the First Step in Dividing Retirement Accounts in Divorce?

The first step is taking inventory. You need to identify every retirement account, confirm what type of plan it is, and gather the records needed to determine what portion may be marital property.

That usually means listing each account, the employer or custodian, the last four digits of the account, and the current balance. It also helps to gather statements from the date of marriage and from the date the court uses to define the marital period, such as separation or filing. If older records are missing, plan administrators may be able to provide historical statements or contribution records.

How Do You Determine the Marital Portion of a Retirement Account?

In many cases, the marital portion includes the contributions made during the marriage and the growth of those contributions. Amounts that existed before marriage, along with any growth tied to them, may remain separate depending on state law.

This is where tracing becomes important. A clear paper trail can help distinguish what was accumulated before the marriage from what was built during it. Payroll records, plan histories, and older account statements may all play a role. For some couples, this is also where professional guidance becomes especially helpful.

What Types of Retirement Plans Might Be Divided in Divorce?

The most common retirement plans fall into a few main categories, and each one is handled differently. Some plans have clear account balances that can be split directly. Others promise future income and must be divided using a formula or future payout election. Knowing which type of plan you are dealing with is essential because the transfer rules, tax treatment, and legal documents can vary significantly.

How Are Defined Contribution Plans Divided?

Defined contribution plans include accounts like 401(k)s, 403(b)s, and 457(b)s. These plans have an individual balance, so division is usually based on either a percentage or a specific dollar amount as of a certain date.

In many cases, the order will also account for investment gains or losses between the valuation date and the actual date of transfer. When handled properly under a qualified order, these transfers can generally occur without current taxes if the receiving spouse rolls the funds into an IRA or another eligible employer plan.

How Are Traditional Pensions Divided?

Traditional pensions are defined benefit plans, which means they pay a future monthly benefit rather than holding an individual account balance. These plans are often divided through a formula tied to the years of service earned during the marriage.

Important details such as survivor benefits and when payments begin should be addressed early. Those elections can materially affect long-term income for one or both spouses.

How Are IRAs and Roth IRAs Divided?

IRAs and Roth IRAs are not usually divided with a QDRO. Instead, they are generally transferred through a process known as a transfer incident to divorce.

The divorce decree should clearly state the amount or percentage to be moved, identify the exact account, and outline the timing. These transfers should be handled directly between custodians, not by withdrawing funds personally and redepositing them later. For Roth IRAs, preserving the five-year clock and basis records is also important.

What Is a QDRO and Why Does It Matter?

A QDRO is a Qualified Domestic Relations Order, and it is often required to divide employer-sponsored retirement plans such as 401(k)s and pensions. Without it, a plan administrator usually cannot legally transfer benefits to a former spouse.

Each plan may have its own model language and review process, and many administrators allow a draft to be reviewed before court approval. That early review can help prevent rejections, rewrites, or delays later. Once the final order is signed, it should be sent promptly to the plan administrator so the transfer process can begin.

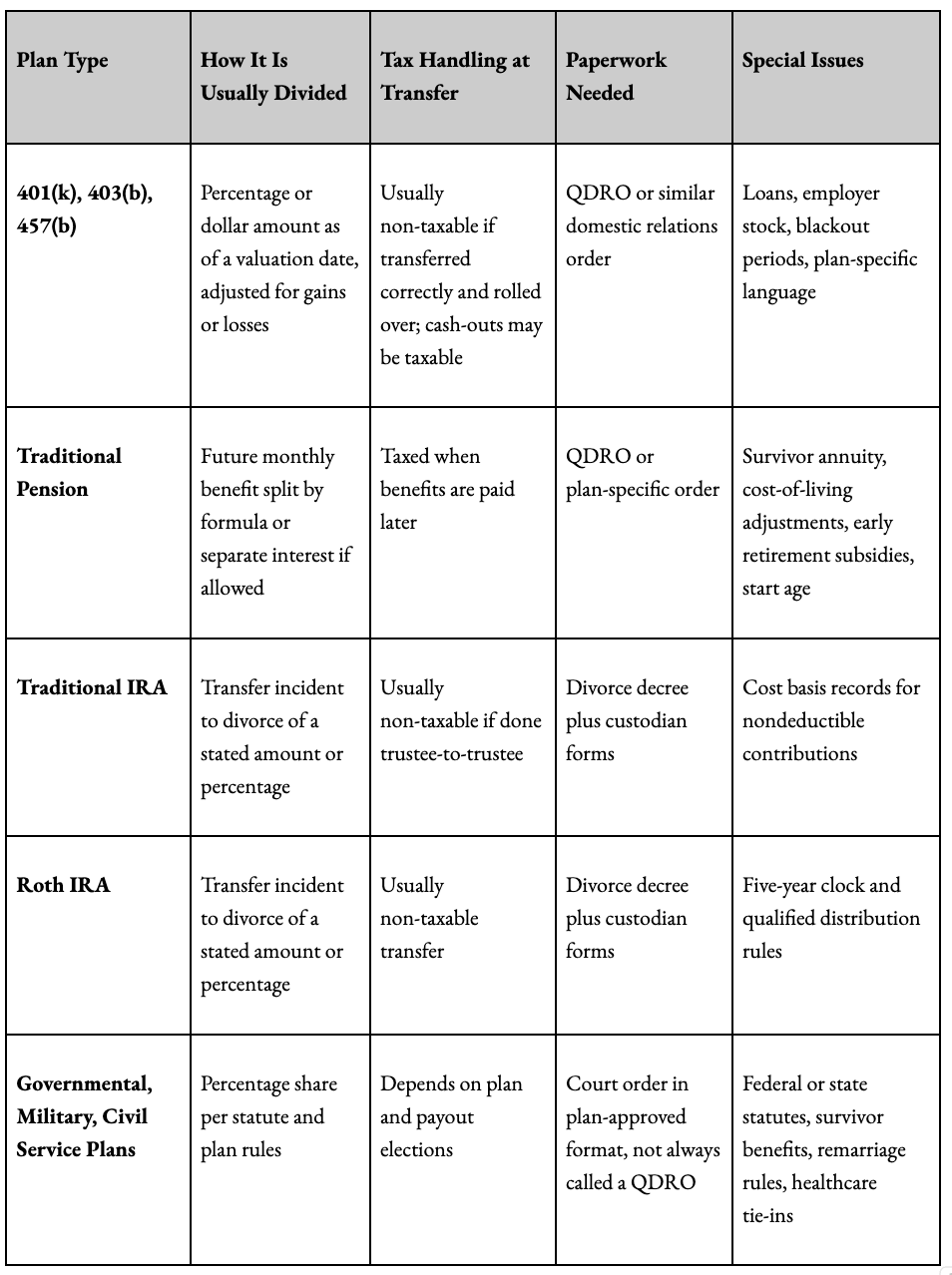

How Are Common Retirement Plans Divided in Divorce?

The right paperwork and tax handling depend on the type of plan involved. A quick side-by-side view can make those differences easier to understand.

Once you know the plan category, it becomes much easier to match it with the proper legal language and administrative process.

Why Do Valuation Dates Matter When Dividing Retirement Assets?

The valuation date is the date used to determine what portion of the account is being divided. It matters because retirement balances can change with contributions, market swings, or plan activity.

For accounts with daily pricing, such as many 401(k)s, the transfer can often be adjusted for gains or losses between the valuation date and the date of actual distribution. Pensions are different because they typically require actuarial calculations rather than daily market values. Before finalizing any order, it is wise to confirm what valuation method the specific plan accepts.

What Tax Issues Should You Watch for in a Divorce Retirement Transfer?

Tax consequences depend on the type of account and how the transfer is handled. That is why process matters just as much as the settlement terms themselves.

- A QDRO transfer from a 401(k) that is paid out in cash is generally taxable as ordinary income.

- A direct rollover to an IRA can preserve tax deferral.

- IRA transfers that are completed correctly as part of a divorce are typically not taxable at the time of transfer, but later withdrawals still follow normal IRA rules.

- Roth IRA taxation depends in part on the five-year holding period for earnings.

- In most cases, direct trustee-to-trustee transfers are the cleanest option.

What Else Should Be Reviewed Besides the Account Balance?

Pensions and retirement plans often involve more than the balance alone. Survivor benefits, beneficiary designations, and even insurance strategies may need attention.

For pensions, survivor elections can affect whether payments continue if one former spouse dies first.

For defined contribution plans and IRAs, beneficiary forms should usually be reviewed and updated after divorce because the decree may not automatically override what is on file.

In some situations, life insurance may also be used to help protect future income.

What Practical Steps Can Help Keep the Process Organized?

A simple checklist can help keep retirement asset division from becoming more confusing than it needs to be. Good documentation often prevents bigger issues later.

Some helpful steps include:

- Gather current statements, plan summaries, and model QDRO language

- Confirm the marital period and the valuation date

- Decide whether the division should use a percentage or a dollar amount

- Address gains, losses, survivor benefits, loans, stock, or other special features

- Seek plan pre-approval when possible

- Coordinate transfers directly between custodians and confirm completion in writing

Staying methodical can make a difficult season feel a little more manageable.

What Common Mistakes Should You Avoid?

The biggest mistakes usually involve delays, vague language, or improper handling of distributions. These errors can lead to rejected orders, taxes, penalties, or transfers that never get completed.

Problems often arise when couples wait until after the divorce to draft the order, fail to update beneficiary forms, or cash out a QDRO distribution without fully understanding the tax impact. Job changes, plan mergers, and administrative shifts can also complicate matters when action is delayed.

What If the Divorce Is Already Final, but the Retirement Transfer Never Happened?

In many cases, there may still be a path forward. If the decree references the retirement plan but the transfer was never completed, the plan’s QDRO department may be able to explain the next steps.

Courts can sometimes issue a post-divorce domestic relations order to enforce the original intent. If the decree never addressed a plan that existed, the available remedies may be more limited, so timely legal advice becomes even more important.

Why Does It Help to Coordinate With a Financial Professional and Other Advisors?

Dividing retirement accounts in divorce is both a legal and financial process. Attorneys, plan administrators, QDRO specialists, and financial professionals each bring a different piece of the solution.

Your attorney helps ensure the language meets legal requirements. The plan administrator confirms what the plan will accept. A financial professional can help you understand values, tax treatment, and how today’s decisions may affect your future goals. When these professionals communicate well, the process is usually more efficient and less stressful.

Frequently Asked Questions About Dividing Retirement Accounts in Divorce

What is the marital portion of a retirement account?

It is generally the contributions and growth earned during the marriage. Pre-marital balances may remain separate depending on state law.

Do retirement accounts get divided by dollar amount or percentage?

Percentages are often safer because they can adjust automatically for market movement between the valuation date and the actual transfer date.

Do you always need a QDRO to divide retirement accounts in a divorce?

No. A QDRO is usually required for employer-sponsored plans like 401(k)s and pensions, but IRAs and Roth IRAs follow different procedures.

Will I owe taxes when I receive my share of a retirement account?

Not usually at the time of transfer, if it is handled correctly through a QDRO or transfer incident to divorce. Cashing out the funds is where taxes often arise.

How long does a QDRO usually take?

Many plan administrators take about four to eight weeks to review and approve a QDRO once it is submitted, though timing varies by plan.

Can a QDRO be issued after the divorce is final?

Often yes. Courts commonly allow post-judgment QDROs to enforce earlier agreements, though acting sooner can reduce complications.

Moving Forward After a Divorce

Dividing retirement assets in divorce can feel mentally and emotionally draining, but it is also one of the most important parts of untangling a shared financial life. These accounts are the result of years of work and discipline, so they deserve careful attention.

A thoughtful process usually comes down to four steps: identify, value, divide, and verify. At Burgdorf Wealth Managers, we believe financial decisions are easier to navigate when they are approached with clarity and wise stewardship.

If you are working through a divorce and want help understanding how retirement assets fit into your broader financial picture, contact our team at Burgdorf Wealth Managers. We’re happy to help you navigate your next steps.